May River Medicare Insurance News & Media Center

This is your hub for Medicare education, media coverage, technology updates, and expert commentary from May River Medicare Insurance. We track what is changing in Medicare across the United States and translate it into clear, practical guidance you can actually use.

Independent Medicare Guidance Nationwide

May River Medicare Insurance is an independent Medicare agency based in Bluffton, South Carolina, serving people turning 65, already on Medicare, and family members helping loved ones across the United States. We work with multiple carriers instead of a single company, which means our loyalty is to you, not to a brand.

Our role is to explain complex Medicare rules in plain language, compare plans in your county and ZIP code, and help you enroll in coverage that fits your doctors, prescriptions, and budget.

Education First, Enrollment Second

Every article, video, and resource we publish is built around one principle: educate first, enroll second. We do not rush appointments, and we do not push a single type of plan.

Instead, we explain the tradeoffs between Medicare Supplement, Medicare Advantage, and Part D plans in language that makes sense. You will find practical insight here on enrollment timing, plan changes, cost trends, and how upcoming legislation may affect your options in the years ahead.

Featured Videos from the May River Medicare Channel

Prefer to learn visually? Our YouTube channel breaks Medicare into short, focused episodes that cover the essentials, common mistakes to avoid, and upcoming changes you need to prepare for.

What You Can Expect

We regularly publish educational videos on:

- Medicare basics for people turning 65.

- How Medicare Supplement, Medicare Advantage, and Part D plans compare.

- Real-world examples of plan reviews and savings opportunities.

- Changes in Medicare law and what they mean for you.

Watch the latest episodes and subscribe to stay ahead of upcoming changes.

Expert Commentary in The Bluffton Sun and Beyond

May River Medicare Insurance regularly contributes Medicare education pieces and opinion columns to local media, including The Bluffton Sun. These articles take national Medicare rules and explain what they mean for people living in South Carolina and across the country.

Medicare Plan Considerations

How to think through your options, compare plans, and avoid rushing into a decision during your initial enrollment window or Annual Enrollment Period.

Medicare Changes in 2026

A look at how upcoming 2026 rule changes may impact premiums, plan design, and the decisions seniors will need to make – and how to prepare ahead of time.

May River Medicare in the Palm of Your Hand

Our mobile app makes it easy to review plan options, request help, and stay on top of your coverage from anywhere in the United States. It is built for people who want simple, secure access to Medicare guidance without spam or pressure.

What You Can Do in the App

- View Medicare plan options in your county and ZIP code.

- Request a call or secure message from a licensed advisor.

- Keep your preferred doctors, prescriptions, and pharmacies handy.

- Receive reminders about enrollment windows and annual reviews.

The app is available nationwide, so you can get help wherever you live in the U.S.

Talk with a Licensed May River Medicare Advisor

When you schedule a one-on-one appointment, you get dedicated time with a licensed, independent advisor whose only job is to help you understand your options. There is no fee, no obligation, and no pressure to choose a particular company or plan.

Complete the Preliminary e-Application

If you already know you will be enrolling or changing plans, you can complete our secure Preliminary e-Application before your appointment. It does not lock you into any plan. Instead, it allows us to have your information loaded, your medications entered, and your local plan options ready to review the moment we start talking.

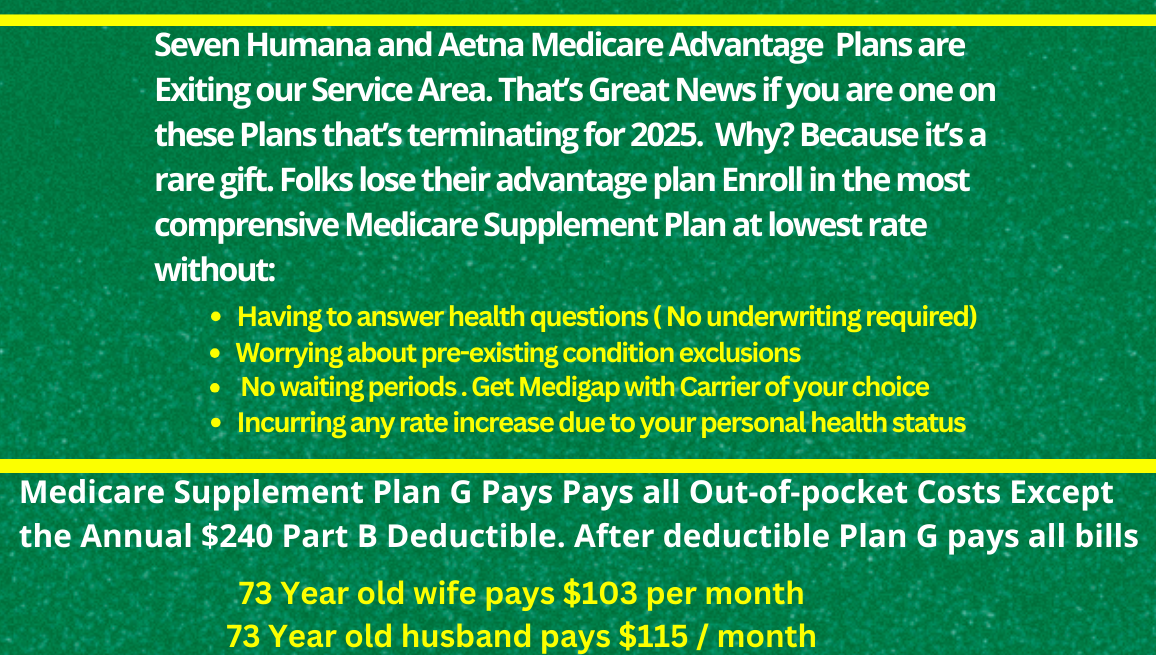

If you have one of the seven medicare advantage plans leaving Beaufort and Jasper County then LISTEN: YOU QUALIFY TO ENROLL IN A MEDICARE SUPPLEMENT AT THE LOWEST RATE WITH THE BEST COMPANY WITH NO HEALTH QUESTIONS OR UNDERWRITING REQUIRED. BY LAW, IF YOUR ADVANTAGE PLAN LEAVES YOUR AREA YOU HAVE A GUARANTEED ISSUE RIGHT: COMPANIES CAN NOT ASK YOU ANYTHING ABOUT YOUR HEALTH AND MUST ISSUE A SUPPLMENT PLAN THAT PAYS ALL YOUR BILLS AFTER MEDICARE DOES.

2025 Medicare Advantage Plans leaner than 2024: Cut Benefits but Increase your Costs while continuing to maximize overpayments by the government.

8 Medicare Advantage Plans Exiting Beaufort Japser for 2025

5 Humana Advantage Plans and 2 Aetna advantage plans leave the Beaufort Jasper county service area. Thousands of folks now have a Guaranteed Issue Right. What does this mean for you?

- 1. Zero Premium plans exit or now Plans with a Premium

- 2. Hospital Stay Costs Increase

- 3. Drug Tier and Formulary Changes: Tier 1 drug now Tier 3 drug.

- 4. Reductions in Dental, Vision, and over the counter benefits

- 5. Unbundling of Benefits means more copays itemized for one procedure such as knee surgery

Lorem ipsum dolor sit amet, at mei dolore tritani repudiandae. In his nemore temporibus consequuntur, vim ad prima vivendum consetetur. Viderer feugiat at pro, mea aperiam

If you are one of the seven medicare advantage plans leaving beaufort or jasper county you can enroll in a medicare supplement with no health questions asked with any company at the lowest rate.

ADVANTAGE PLAN LEAVING OUR AREA

- Guaranteed issue rights, also known as Medigap protections, are rights that allow people to purchase certain Medicare Supplement (Medigap) plans without medical underwriting.

- This means that insurance companies must offer coverage for pre-existing health conditions and cannot charge higher premiums due to health problems.

- If you have an advantage plan that is terminating, you can either enroll in a Plan G supplement or Plan F WITH NO HEALTH QUESTIONS OR UNDERWRITING ALLOWED. Your are guaranteed a medicare supplement with to be issued to you with any company at the lowest rate. (Use an Independent Broker licensed with all or most of the companies to get best rate.)

Massive Changes to Part D Drug Plan

Big Changes to the Medicare Prescription Drug Plan beginning in 2025. Who will benefits and who will lose from the Medicare Part D 2025 Changes. The changes are a Godsend for the minority of folks on expensive drugs, but for most, be prepared. Since the insurance companies not medicare or the Pharmaceutical Companies now incur the heavy cost burden of paying for drugs in 2025, be ready for the insurance company to make that money back by using tier and formulary changes next year, so open your annual notice of change, because the times they are a changing and soon.