Medigap Plan C

High-Coverage Supplement

Medigap Plan C is one of the most comprehensive Medicare Supplement plans ever offered, covering nearly all out-of-pocket costs left by Original Medicare.

Important: Medigap Plan C is only available to people who became eligible for Medicare before January 1, 2020.

May River Medicare Insurance is a nationwide independent Medicare agency. We clearly show plan availability, pricing, and eligibility rules by ZIP code — before you speak to anyone. Full transparency. Nationwide reach.

Plan C covers most Medicare deductibles, copays, and coinsurance amounts.

Only available to beneficiaries eligible for Medicare prior to 1/1/2020.

No networks — see any provider nationwide that accepts Medicare.

Plan C includes all benefits from Plans A and B, plus additional cost-sharing protection.

- Part A hospital deductible

- Part A hospital coinsurance and extended stays

- Part B coinsurance (the 20%)

- Part B deductible

- Skilled Nursing Facility coinsurance

- First 3 pints of blood each year

- Hospice coinsurance/copayment

- Foreign travel emergency benefit

- Prescription drugs (Part D is typically needed)

- Routine dental, vision, or hearing care

- Long-term custodial care

- Any services not approved by Medicare

Due to federal law changes, Medigap Plan C is closed to people who became eligible for Medicare on or after January 1, 2020. If you qualify, Plan C may still offer one of the highest levels of coverage available.

- Must have Medicare eligibility prior to 1/1/2020

- Carrier availability varies by state and ZIP code

- Medical underwriting may apply outside protected enrollment periods

See If You Qualify for Medigap Plan C

If you’re eligible for Plan C, compare carriers and pricing in your county. May River Medicare Insurance helps you verify eligibility, compare options, and enroll with confidence — all with full transparency.

Medicare Plan C

is the most basic Medicare Supplement.

Medigap Plan C Benefits

Your hospital deductible is a per-incident deductible, not an annual one, so this is an important benefit. Medicare Plan B will pay the deductible even if you incur it more than once in the same year.

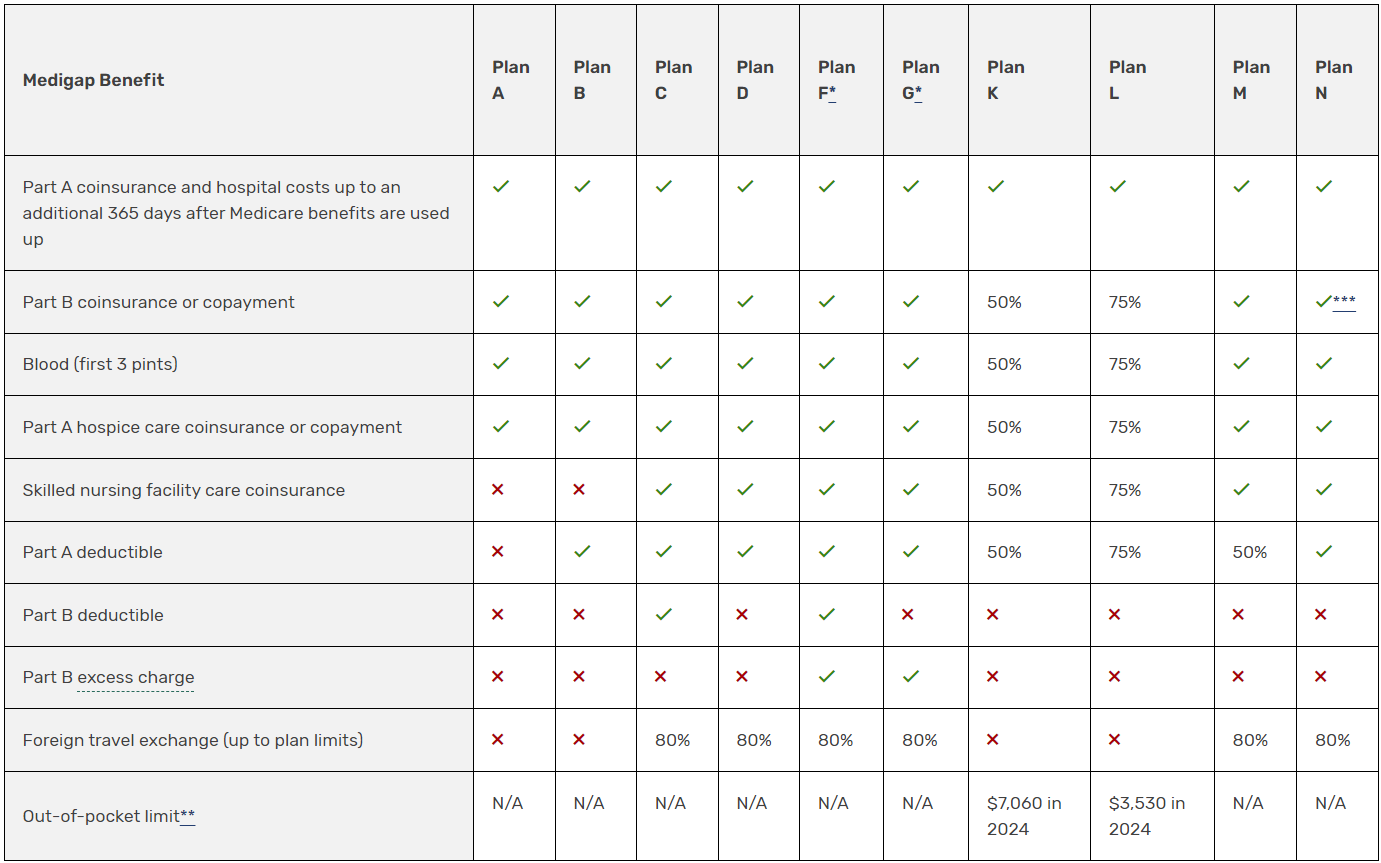

The chart below shows basic information about the different benefits Medigap policies cover.

✔ = the plan covers 100% of this benefit

X = the plan doesn’t cover this benefit

% = the plan covers that percentage of this benefit and you’re responsible for the rest

N/A = not applicable

The Medigap policy will only pay your coinsurance after you’ve paid the deductible (unless the Medigap policy also covers your deductible).

Excess charges are surcharges your doctor can charge above and beyond what Medicare will reimburse. They are limited to 15% beyond what Medicare pays. Many doctors do not charge excess charges, but occasionally they do. If this concerns you, then Medigap Plan F or G might be a better choice for you than Medicare Plan C. Those two plans cover excess charges, so you won’t have to worry about asking.

Consider this scenario: Adrian purchases a Medigap Plan C policy. Most of his doctors are participating Medicare doctors so Adrian usually owes absolutely nothing. Adrian twists his ankle while walking his dog. Then he notices swelling, so he visits an urgent care clinic for an X-ray. The clinic does not accept Medicare assignment rates but chooses to bill an excess charge. The fee for the X-ray is normally $50 but at this clinic there is a 15% excess charge, bringing the cost to $57.50. Since Adrian’s Medigap Plan C does not cover excess charges, Adrian will owe the $7.50 difference to the medical facility.

Medicare Plan C is one of 10 different Medicare Supplement options available to you. (Part C, on the other hand, refers to Medicare Advantage policies. These are not Supplements and work very differently than Supplements.) If you buy a Plan C, you will enjoy the freedom of access to top physicians and hospitals that you already get with Original Medicare. You can also rest easy that your Supplement policy will pay for things like your inpatient and outpatient deductibles. This has made it a popular seller for decades.

Again, Medicare Plan C has benefits very similar to Plan F. So, if not having the coverage for excess charges worries you, then you might consider quotes for the F policy for comparison. You will find that in many areas the prices are nearly equivalent, making it quite cost-effective to buy the richer coverage if that appeals to you.

- Although Plan C covers everything but Part B excess charges, it’s not cost-effective for some as its monthly premiums may be too high. If this is the case for you, you may consider Plan N or Plan G instead.

- If you’re unsure if Plan C is a good fit for you, feel free to give our team a call at 817-249-8600 for free assistance.

Get your Personalized Quote in Seconds without the annoying calls afterwards.

We’ve got representation available in

all 43 states.

May River Medicare beneficiaries are served in 43 states. Unlike other agents and brokers, we provide lifelong support for your policy and deliver exceptional customer service.